41% of Americans Who’ve Never Owned a Home Believe 20% Down Payments Are Required — And It Could Be Holding Them Back From Homeownership

Many Americans dream of owning a home, but prospective first-time buyers face numerous hurdles — particularly with down payments. The latest LendingTree survey of more than 2,000 U.S. consumers finds that the majority of would-be homeowners stress about affording a down payment, and common misconceptions about how much they should put down may be holding them back.

According to LendingTree senior economic analyst Jacob Channel, prospective first-time buyers don’t necessarily have to put their white picket fence plans on hold until they meet a certain threshold for down payments. Many homeowners didn’t, he says.

“There’s no magic number for how much a person should put toward a down payment,” Channel says. “Twenty percent is often considered ideal, but most people put down closer to 10% or less, which goes to show that you can still get approved for a mortgage even if you can’t reach 20%.”

Key findings

- Down payments hold back many from homeownership. 81% of prospective first-time buyers are stressed about affording a down payment. Further, 27% of those who’ve never owned a home but would like to say that down payments are the main barrier holding them back from homeownership. An additional 49% say down payments are one of many barriers.

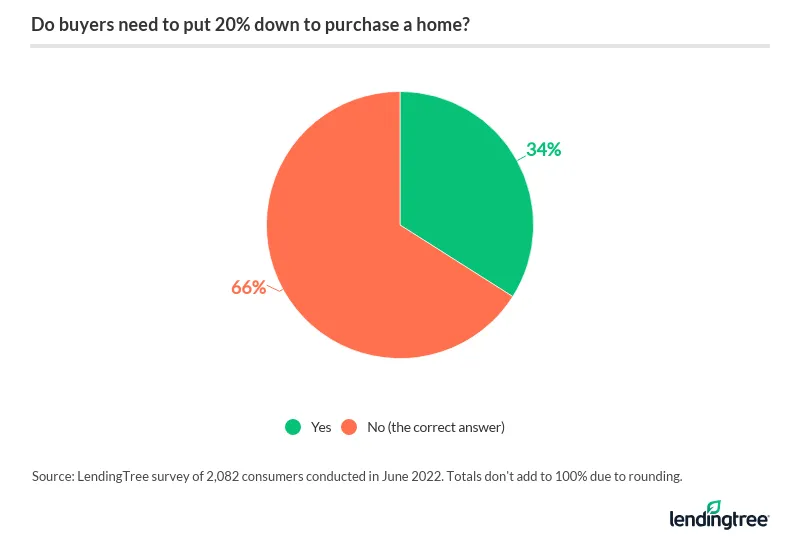

- Misconceptions about how much a consumer should put down may be an additional barrier. More than a third of Americans — and 41% of those who’ve never owned a home — believe they must put down 20% to buy a home. However, an April 2022 report from the National Association of Realtors found that 44% of homebuyers put down less than 20%.

- Private mortgage insurance (PMI) can be confusing, and many Americans (60%) have no idea how to get rid of it. That could be because rules vary by lender — for example, some lenders will remove PMI by request once your loan balance reaches 80% of the home’s purchase price, while other lenders require you to refinance first. Still, 50% of Americans don’t want to put down less than 20% because they don’t want to owe PMI, which is required for lower down payments.

- Nearly a quarter (24%) of homeowners say their loved ones helped with their down payment, either as a gift (16%) or loan (8%). This surges to 37% among millennial homeowners. Among those who’ve never purchased a home but hope to do so, 21% expect financial assistance from family or friends.

- Nearly 30% of prospective first-time buyers hope to finance their down payment with a personal loan — but most lenders don’t allow this. Personal loans are prohibited as a down payment source for conventional and Federal Housing Administration (FHA) mortgages.

Prospective homeowners stress about down payments

There are many reasons why homeownership may feel out of reach for the average American, though consumers are generally inclined to believe costly down payments prevent them from homeownership. More than a quarter (27%) of those who’ve never owned a home — but want to say — they’d already have one if they didn’t have to worry about saving for down payments. An additional 49% say saving for a down payment is just one barrier among many.

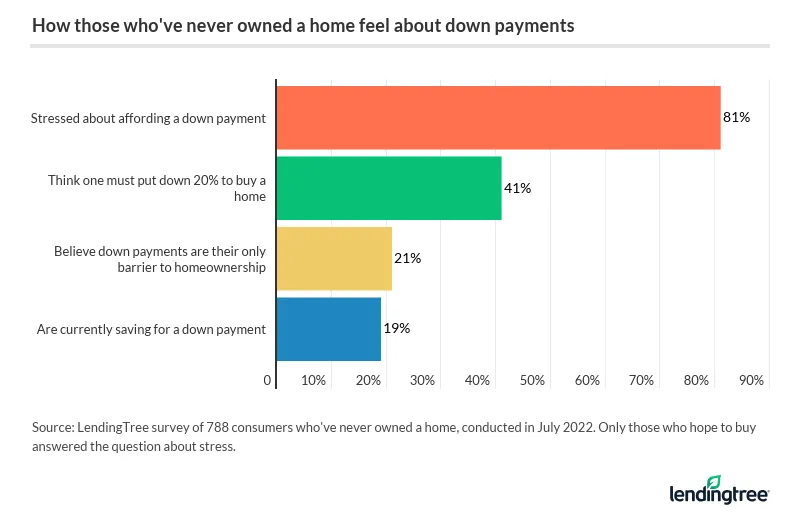

Consumers who hope to buy a home are particularly concerned about future down payments. Nearly two-thirds (65%) of those who’ve never owned a home say they’d like to be a homeowner one day. But among prospective first-time buyers, 81% are stressed about affording a down payment. Baby boomers ages 57 to 76 (86%) and those with household incomes of less than $35,000 (86%) are the most likely to feel stressed.

Those who hope to own a home have high goals, too. Just over 4 in 10 (42%) prospective first-time buyers say they expect to put down at least 20%. Still, most prospective first-time homebuyers haven’t started saving for their down payment yet. In fact, just 19% of those who’d like to own a home but never have say they’re currently saving for a down payment. While six-figure earners are the most likely to be saving for a down payment (41%), millennials ages 26 to 41 (24%) and Westerners (21%) are also more likely to be saving up.

Those who aren’t saving for a home may have a long way to go, as 53% of homeowners who financed their down payments with savings put aside specifically for that reason say it took them three or more years to save up for it. For Northeasterners (36%) and Gen Xers (35%), it took five or more years.

More than a third of Americans believe 20% down payments are necessary

One factor contributing to down payment stress may be consumers’ misconceptions about how much they need to put down. Overall, 34% of Americans believe they must put down 20% to buy a home. Among those who’ve never been homeowners, that percentage jumps to 41%.

In reality, however, a 20% down isn’t a requirement. It’s merely a goal, and it’s one not all homeowners reach. In fact, 44% of homebuyers put less than 20% down, according to an April 2022 confidence index survey from the National Association of Realtors (NAR).

While Channel cautions that smaller down payments don’t come without risks, he says prospective homeowners shouldn’t fixate on hitting the 20% figure simply because they think they need to do so.

“A smaller down payment may make it harder for you to get approved for a loan, and it might also result in getting a higher interest rate if you’re approved,” Channel says. “With that said, because so many homeowners put less than 20% down, most would-be homebuyers probably don’t need to worry too much about not being able to put 20% or more down.”

He adds that prospective homeowners should still aim for high down payments — as long they leave enough cash for future expenses. As a general rule, buyers should consider what their monthly mortgage payments might look like to determine the down payment amount that best fits their long-term needs.

Down payment expectations versus reality among homeowners

Experience can be the best teacher. While prospective first-time buyers have high expectations for their down payment amounts, looking at what homeowners put down (and if they wished they put down more) may offer some insight.

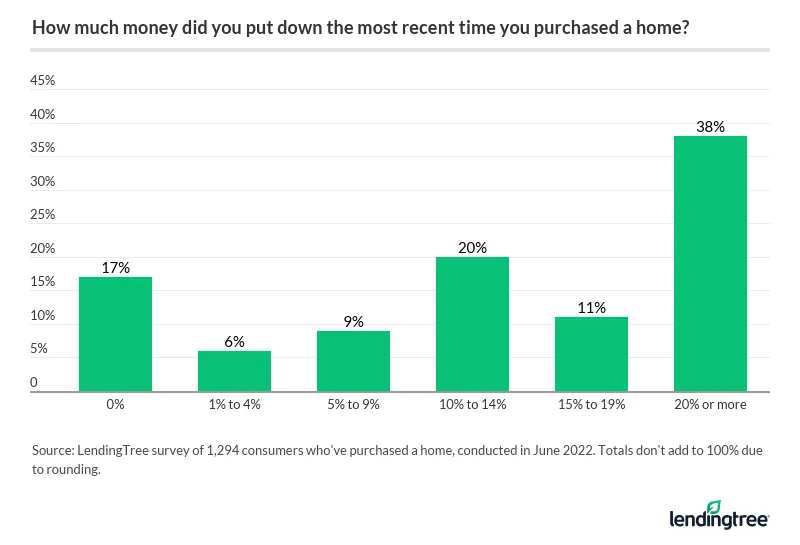

Almost 4 in 10 (39%) consumers who’ve owned a home say they expected to put 20% down. That generally aligns with what they put down, too, as 38% of homeowners in the LendingTree survey say they put down 20% or more.

But that varies by demographic. Overall, older consumers are more likely to meet their down payment expectations than younger consumers. More than half (51%) of baby boomers say they expected to put down 20% or more — the highest of any group — and the same percentage did just that. Meanwhile, 42% of Gen Xers had similar expectations, but only 36% met them.

Overall, millennials are less likely to do either. The percentages of those who expected to make such high down payments and those who did were both 27% — 24 percentage points lower than baby boomers.

Despite whether they met their expectations, 30% of homeowners wish they’d put more toward their down payments — particularly millennials (44%) and Northeasterners (37%). Notably, just 24% of homeowners making less than $35,000 annually feel similarly.

Many Americans don’t know how to get rid of private mortgage insurance

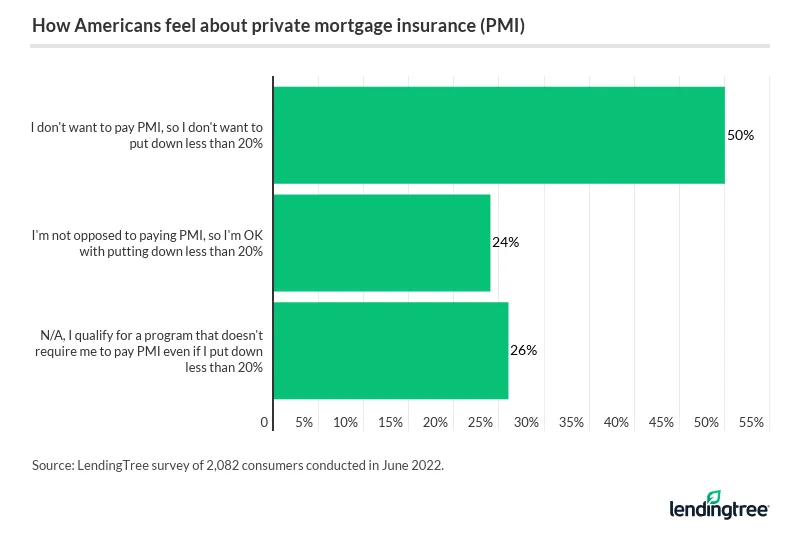

Private mortgage insurance (PMI) — an extra insurance policy designed to protect lenders — might influence Americans’ opinions toward the 20% figure. Across all respondents, half (50%) say they wouldn’t want to put less than 20% down on a home because they wouldn’t want to owe PMI, which is generally required for those who can’t pay 20% on a conventional loan.

But most consumers’ fears may simply stem from a lack of knowledge. Overall, 60% say they have no idea how to remove PMI. An additional 34% believe that it has something to do with reaching 20% in home equity, but they’re split on how it works: 17% believe PMI automatically goes away at this point, and another 17% say homeowners have to refinance their mortgages to remove PMI.

There is some truth in consumers’ beliefs. While the process varies by lender, all lenders are legally required to stop charging PMI once a loan balance reaches 78% of the home’s purchase price — which is notably different from home equity, as it prevents homeowners from taking advantage of a hot market or making improvements to their home to remove PMI. Still, Channel notes that homeowners can utilize home equity to get rid of PMI, too.

“You may also be able to get your PMI removed by simply calling up your lender and asking them to cancel it once your loan balance has reached 80% of your home’s value,” he says. “Though if you do this, your lender may require you to pay for an appraisal just to be sure you really have built as much equity into your home as you say you have.”

Other government-backed loans are another matter entirely. While Federal Housing Administration (FHA) loans don’t require PMI, they do require upfront and annual mortgage insurance premiums (MIPs). Unlike those with PMI, borrowers are required to pay annual MIPs for as long they have the loan. The only exception is if a borrower puts more than 10% down on an FHA loan — in this case, it’ll go away after 11 years. Otherwise, refinancing is the only way to get rid of an MIP.

For those utilizing housing assistance programs, U.S. Department of Veterans Affairs (VA) loans don’t require PMI.

Financing: Homeowners vs. prospective homeowners

Prospective first-time buyers’ expectations vary from homeowner experiences beyond just down payment amounts. How they plan to finance their down payments is also different. Overall, saving money is the most popular method: 64% of prospective first-time buyers plan to save up specifically for this purpose — among homeowners, 55% used savings for their down payments.

Among homeowners, millennials (63%) and Northeasterners (60%) were the most likely to put their savings toward a down payment, and male homeowners (61%) were much more likely to do so than female homeowners (47%). Meanwhile, some prospective buyers are significantly more likely to expect they’ll pay with savings — particularly those with household incomes of $75,000 to $99,999 (74%), Gen Zers ages 18 to 25 (74%) and Northeasterners (70%).

Homeowners also relied on help from their loved ones, though prospective buyers aren’t as likely to think they’ll do the same. Nearly a quarter (24%) say their loved ones helped with their down payment — either as a gift (16%) or loan (8%) — making it the second most common financing method for homeowners. Comparatively, 21% of prospective buyers expect assistance from family or friends. Though this isn’t a significant drop, the disparity is most notable among millennials: 37% of homeowners in this age group relied on loved ones to help with their down payments, while just 19% of would-be owners expect to do the same.

Though a loved one’s support may relieve prospective homeowners from many financial stressors, Channel warns that they should be aware of what gifts or family loans entail.

“Be sure you understand the tax implications of being given money for a down payment,” Channel says. “If an individual gets a cash gift worth more than $16,000, they need to report it to the IRS. Usually, the donor is responsible for gift taxes, but sometimes the recipient might be the one on the hook.”

He adds that buyers should be sure they’re open with their lender about where their funds are originating, as some lenders may require buyers to take additional steps (like filling out extra paperwork) if they plan to use a gift to make a down payment. And to some lenders, using a loan from a friend or family member to pay for a down payment could be seen as mortgage fraud.

Nearly 30% of prospective buyers want to finance down payments with personal loans

In light of some mortgage loan restrictions, some would-be buyers may need to reconsider their financing options. More than a quarter (27%) of prospective first-time buyers hope to finance their down payment with a personal loan, making it the second most popular option overall. However, conventional and FHA mortgages prohibit consumers from using personal loans to fund their down payments.

Still, alternative mortgage programs exist, so it isn’t impossible to finance a down payment through a personal loan — in fact, 10% of homeowners did precisely that — but it’s usually not recommended. Beyond limiting a buyer’s loan options, the downsides of using a personal loan include high interest rates and potential impacts on a homebuyer’s credit score.

However, for prospective buyers who are still determined to finance their down payments through a personal loan, there are some ways to do it right. When choosing the right personal loan, some factors to consider include:

- APR rates. Your APR is how much you borrow, plus interest. Those seeking a personal loan should shop around to find loans with the lowest APRs.

- Fees and penalties. Some lenders charge origination fees, which are typically 1% to 8% of the loan balance. In addition, most don’t charge prepayment penalties for paying off a loan early, though some will.

- Minimum credit requirements. Some lenders have stricter credit score requirements for borrowers than others. In general, the higher your credit score, the more competitive your interest rate could be.

For the pros and cons of using a personal loan to finance down payments, read our guide.

The best financing option? Save, save, save

Financing down payments can certainly be a challenge. Last year, the average cost of a down payment in the largest 50 U.S. metros was over $46,000 — which isn’t exactly cheap. Still, Channel says it’s certainly within reach for those who dream of homeownership.

In fact, he recommends that prospective buyers begin planning for future down payments now.

“Though it’s often easier said than done, the best way to finance a down payment is to start saving as much as you can as soon as possible,” Channel says. “Remember that the more time you give yourself to save for a down payment, the more money you’ll likely end up with when it comes time to finally get a loan and purchase a home.”

For those who hope to become homeowners, Channel believes small steps can have a big impact in the long run. While making a budget is a vital first step, cutting back on nonnecessities like eating out or vacationing can help save money. Alternatively, he suggests seeking a lower-cost place to live while gearing up to buy a home, like temporarily moving in with roommates or family.

Of course, consumers don’t necessarily need to do it all themselves, either. Low-income and military homebuyers may not have to put any money down; the VA and U.S. Department of Agriculture (USDA) loan programs offer low- or no-down mortgages, though some restrictions exist. In addition, down payment assistance programs — such as grants or second mortgages — can offer valuable support for eligible people.

Methodology

LendingTree commissioned Qualtrics to conduct an online survey of 2,082 U.S. consumers, fielded June 10-14, 2022. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2022:

- Generation Z: 18 to 25

- Millennial: 26 to 41

- Generation X: 42 to 56

- Baby boomer: 57 to 76

While the survey also included consumers from the silent generation (those 77 and older), the sample size was too small to include findings related to that group in the generational breakdowns.

View mortgage loan offers from up to 5 lenders in minutes