Nearly 40% of Americans Say Their Financial Situation Is Closer to the Worst Than the Best

“It was the best of times, it was the worst of times … ”

The iconic opening line of Charles Dickens’ “A Tale of Two Cities” was published in 1859, but the description of that era’s extreme contradictions is a pretty apt summary of the financial lives of Americans today.

For many — nearly 40% — it’s the worst of times for their personal finances rather than the best, according to the latest LendingTree survey of 2,000-plus Americans.

Read on for more about how Americans are coping with the current financial climate and tips on navigating its challenges.

Key findings

- Although the U.S. economy appears to be on the upswing, many Americans still reel from years of turbulence. 38% of Americans say their financial situation is closer to the worst than the best, while half of consumers feel financially unstable. Additionally, a higher percentage of Americans are pessimistic about the economy (38%) than optimistic (34%).

- Some consumers are struggling to stay afloat, pointing the finger at inflation. 37% of Americans are behind on monthly bills, which jumps to 53% among parents with young children. Americans are most behind on credit card (19%), recurring bill (13%) and rent (10%) payments. Additionally, 61% report inflation has impacted their ability to afford their lifestyle.

- While many Americans think their finances are at a personal low, brighter days could be ahead. 45% say they’re optimistic about their finances in the next year, and 43% expect their income to increase in that period. However, 56% of Americans are worried about a recession in the next year.

- More news may lead to more problems. The overwhelming majority (86%) of Americans follow news related to the economy. It’s influencing their financial outlook, as 94% of them say it affects their perception of the economy. When asked where they consume this information, 68% said they turn to television for news, 55% utilize online news sources and 46% cite social media.

- In a presidential election year, views on the economy differ. Democrats are significantly more optimistic than Republicans about the economy (51% versus 28%), and Republicans are more worried about a recession than Democrats (69% versus 48%). Additionally, Republicans are more likely than Democrats to say their finances are closer to the worst they’ve been (42% versus 31%).

Worst-case scenarios don’t always bring out the best

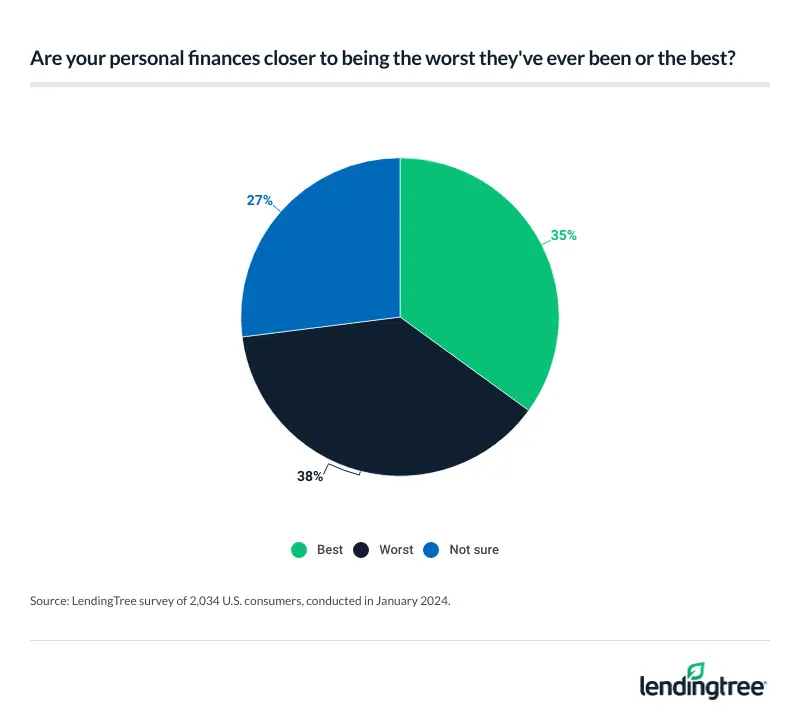

The economy may be improving, but many Americans are down about their financial situation. When asked if their personal finances are closer to the worst they’ve been or the best, 38% said theirs are closer to the worst, 35% said theirs are closer to the best and 27% said they’re unsure.

For some, it’s worse than others:

- More women than men say it’s the worst of times for their finances — 42% versus 33%.

- Older generations are more likely to say it’s the worst of times for them — 41% of Gen Xers ages 44 to 59 and 39% of baby boomers ages 60 to 78, versus 38% of millennials ages 28 to 43 and 32% of Gen Zers ages 18 to 27.

- Politically, 44% of independents, 42% of Republicans and 31% of Democrats say it’s the worst of times for their personal finances.

But how do you know if you’re closer to your best or worst financial state?

In some ways, it’s simple to quantify, according to Matt Schulz, LendingTree chief consumer finance analyst. He says things like your net worth and overall debt level provide a dollars-and-cents look at where you stand. But it’s not always cut and dry.

“Maybe you’ve paid down your debts and raised your net worth a bit, but you feel like you’re still struggling to make ends meet and get ahead,” Schulz says. “Maybe you’re nervous about your job security as you’re about to send a kid to college. Maybe your health has taken a major turn, and you’re scared of what’s ahead, physically and financially. Or, on the flip side, maybe you’re still in a difficult place but know you’ve turned the corner for the first time in years. All these things can affect your perspective on your financial situation.”

So how are Americans feeling about their finances? In a word, shaky. Overall, half of respondents say they don’t feel financially stable:

- More women are likely to report feeling financially unstable than men — 56% versus 44%.

- 56% of Gen Xers say they feel financially unstable, compared with 52% of millennials, 45% of Gen Zers and 43% of baby boomers.

- More independents report feeling financially unstable (55%) than Republicans (49%) and Democrats (42%).

Optimism isn’t running especially high either, as 38% of Americans say they’re pessimistic about the state of the economy. Only 34% say they’re optimistic, while 28% say they’re neutral. Further:

- Women report more pessimism than men — 44% versus 33%.

- Older generations are more pessimistic than their younger peers — 47% of baby boomers and 42% of Gen Xers, versus 32% of millennials and 32% of Gen Zers.

Americans are struggling with monthly bills, and many say inflation is impacting their lifestyle

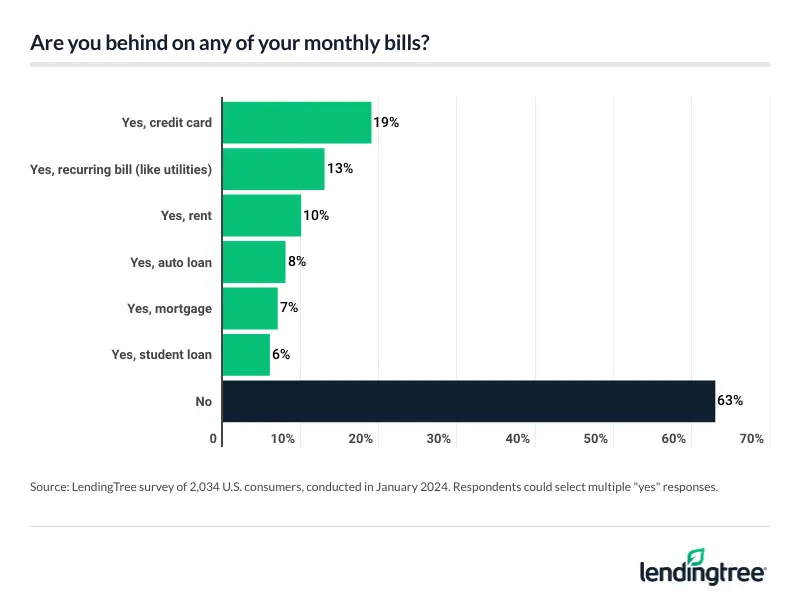

Those shaky feelings aren’t necessarily unfounded either, as 37% of Americans are behind on their monthly bills — bills that often carry steep interest rates, penalties and other repercussions when unpaid. That rate jumps to 53% among parents with young children.

Which bills? Credit cards (19%) top the list, followed by recurring bills (13%) and rent payments (10%).

More people may join the ranks of those behind on their bills in the coming months. Of those who say they’re not behind on any bills, 9% think they will fall behind in the next six months. That rate jumps to 11% among parents with young children.

Beyond bills, inflation may limit Americans’ overall manner of living, with 61% saying inflation impacts their ability to afford their lifestyle. Again, parents with young children are seemingly hit even harder than average, with 69% saying inflation impacts their ability to pay for their lifestyle.

So what’s the answer? Buckle up and budget for it with the assumption inflation isn’t going away anytime soon, Schulz says. “Yes, inflation seems to have peaked, but it hasn’t gone away. Your best move is to adjust your budget accordingly, assuming your expenses over the next six to 12 months will be a bit higher than today. Far better to prepare for the worst in your budget and be pleasantly surprised than the other way around.”

Are consumers singing about better days?

If they’re singing, the volume is faint. Fewer than half (45%) of Americans say they feel optimistic about the state of their finances in the next year. Some have rosier outlooks on their personal finances than others:

- More men report feeling optimistic about their finances than women — 51% versus 40%.

- Democrats (56%) are more optimistic about their finances than Republicans (43%) and independents (41%).

- People with small children (49%) are more optimistic than those with children 18 and older (44%) or no children (43%).

Is more money on the horizon? An optimistic 43% say they expect to see their income increase this year, but 47% say they expect their income to decrease or stay the same this year.

Are there ways they can change their income now? It’s rarely easy, but there are options.

“It’s never been easier to start a side hustle or a small business,” Schulz says. “Unemployment is still relatively low, so it might be possible to move to a higher-paying job. You can also try to pursue a raise in your current job. What people need to understand is that these options aren’t going to be thrown at their feet. You have to go after them.”

People can also consider the other side of the financial equation and lower their expenses. Depending on the gravity of your situation, it may just require canceling some streaming services and dining out less, or you may have to do something more serious, but it’s worth considering.

Is a recession another looming threat? More than half (56%) of Americans are worried about one hitting in the next 12 months.

Who’s the most worried?

- 59% of women, versus 53% of men.

- 59% of Gen Xers, versus 58% of millennials, 53% of baby boomers and 50% of Gen Zers.

- 62% of people with young children, versus 56% of people with children 18 and older and 51% of people with no children.

Do you want the good news or the bad news?

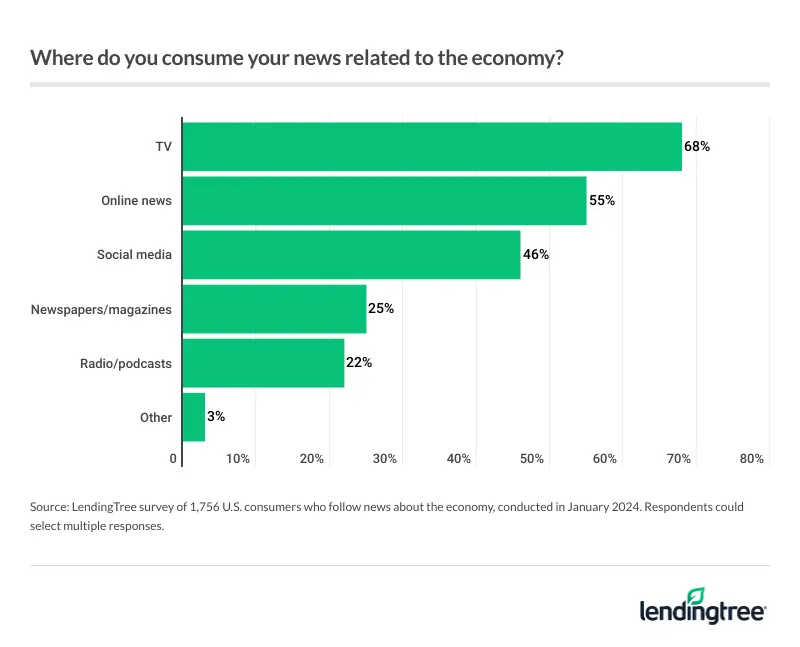

Americans aren’t burying their heads in the sand when it comes to news about the economy. The vast majority (86%) say they follow it at least to some degree. Most of those who follow it say they keep up via television (68%), while 55% consume news online and 46% get news on social media.

Does the news affect people’s perception of the economy? Of those who follow it, 94% say it does … for better or worse.

Schulz says following economic news comes with pros and cons. On a positive note, it can help you see hurdles, such as rising interest rates, coming so you’re not blindsided. But paying too much attention to it can be damaging because it may lead you to focus on things out of your control.

“The truth is that you are better off focusing on things that you can control, such as your income and spending, than focusing on things that you can’t do anything about,” he says.

Views on economy differ in presidential year

Different parties have different perspectives on the economy and personal finances. Overall, Democrats seem to see the sunniest financial skies.

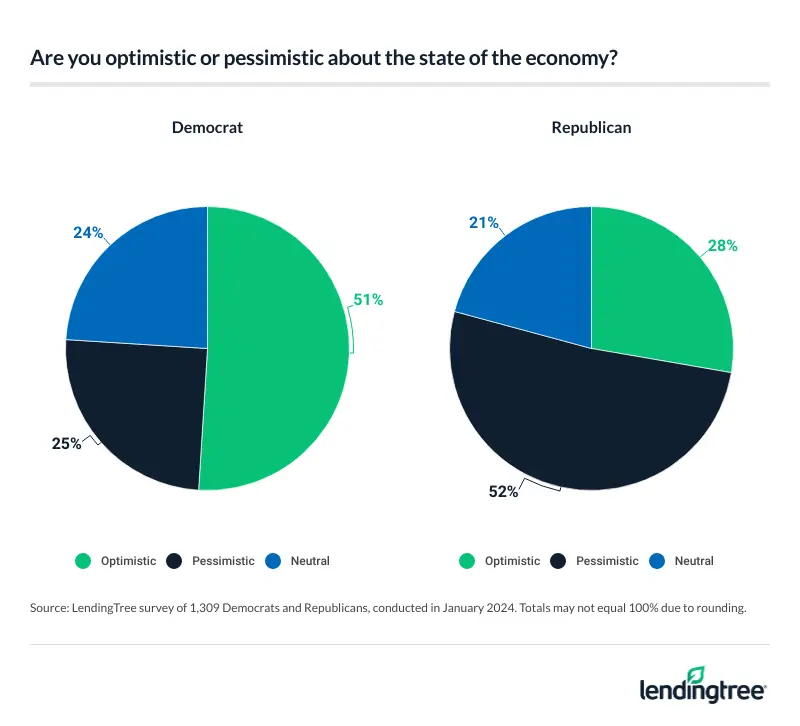

Members of the blue party are the most optimistic about the economy. In fact, Republicans are twice as likely to report feeling pessimistic about the economy as Democrats — 52% versus 25%, respectively. Independents fall in between, with 43% reporting pessimism about the economy.

Republicans’ trunks are twisting with anxiety about a recession, as 69% say they’re worried about one hitting in the next 12 months, while only 48% of Democrats say the same. Again, independents hold the middle ground between the two, with 54% worried about a recession.

And it’s personal, too. As mentioned earlier, independents (44%) are the most likely to say their personal finances are closer to the worst of times than the best. They’re followed by Republicans (42%). Democrats trail behind, with 31% saying it’s the worst of times for their finances.

4 tips to overcome financial hurdles

If you’re leaning more toward the worst of financial times or fearing they’re to come, there are things you can do to brace for and overcome the hurdles. Here are four:

- Budget, budget, budget. A well-thought-out budget can help you navigate tough financial times because it lays out everything on the table. It may not be fun to put together and maintain, but it matters.

- Keep saving while paying down debt. This may be easier said than done, but it’s crucial. Continuing to save when paying down debt is the key to breaking the cycle of debt that so many people find themselves in. Yes, it means it may cost a little more and take a little longer to pay the debt off, but it also means you’ll have a cushion of savings when you’re done. That means the next unexpected expense after you get your credit card debt down to $0 won’t have to go right back on your card. That’s a big deal.

- Manage interest. If people are struggling with high interest rates, they don’t have to wait for the Federal Reserve to act. They have many options of their own, especially if they have good credit. A 0% balance transfer credit card is about the best tool that people have in the fight against credit card debt, but a low-interest personal loan can be great, too. Also, people can call their card issuer and ask for a lower interest rate on their credit card. They’re far more likely to get their way than they might realize.

- Expand your income. Whether looking for a new, higher-paying job, asking for a raise or taking on a side hustle, search for ways to boost your income. More money is rarely going to just fall into your lap. But with some creativity and hard work, there are almost always ways to bring in more.

Methodology

LendingTree commissioned QuestionPro to conduct an online survey of 2,034 U.S. consumers ages 18 to 78 from Jan. 17 to 19, 2024. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. Researchers reviewed all responses for quality control.

We defined generations as the following ages in 2024:

- Generation Z: 18 to 27

- Millennial: 28 to 43

- Generation X: 44 to 59

- Baby boomer: 60 to 78

Get debt consolidation loan offers from up to 5 lenders in minutes